🍁 Commercial Solar Incentives in Canada: a Full Guide

If you’re researching commercial solar incentives in Canada, the biggest mistake is looking at “one rebate” instead of the full incentive stack. For many businesses, commercial solar becomes dramatically more attractive when you combine:

- Federal refundable tax credits (like the Clean Technology Investment Tax Credit)

- Accelerated depreciation (CCA) to improve after-tax cash flow

- Utility/export credit programs (net metering / net billing / self-generation) that determine how your savings actually show up on the bill

This guide walks you through the incentives that matter most for ‘commercial solar in Canada’, how they fit together, and what your accountant typically needs to claim them properly. (Not tax advice — always confirm specifics with your tax professional.)

✍️ Quick takeaway (plain English)

Commercial solar ROI usually improves when you:

- ✅ Reduce upfront cost through refundable credits,

- ✅ Accelerate tax deductions through CCA, and

- ✅ Design the system around your utility’s export rules (so the savings are real, not just “on paper”).

🍁The 2026 Commercial Solar Incentive Stack (60-second overview)

Here’s the “stack” most commercial buyers should understand:

1) Clean Technology Investment Tax Credit (CT ITC)

A refundable federal tax credit that can return a meaningful portion of eligible project costs — often the headline incentive that changes the economics.

2) Capital Cost Allowance (CCA) for clean energy equipment

Solar can often qualify under clean energy CCA classes (your accountant will determine the correct class). CCA is about improving after-tax cash flow by deducting more sooner instead of slowly over time.

3) Utility export / credit rules

Your province/utility program determines whether exports become bill credits (kWh or dollars), how long credits carry, and how annual true-ups work. This is why two identical solar systems can perform very differently financially in different provinces.

If you want a fast “business-case” estimate, MAG Solar can build a preliminary view based on your load, site constraints, and the incentive stack that fits your location.

But if you're thinking about making the switch, you likely have some important questions:

This comprehensive guide will answer all your questions and walk you through everything you need to know about Commercial Solar Incentives in Canada

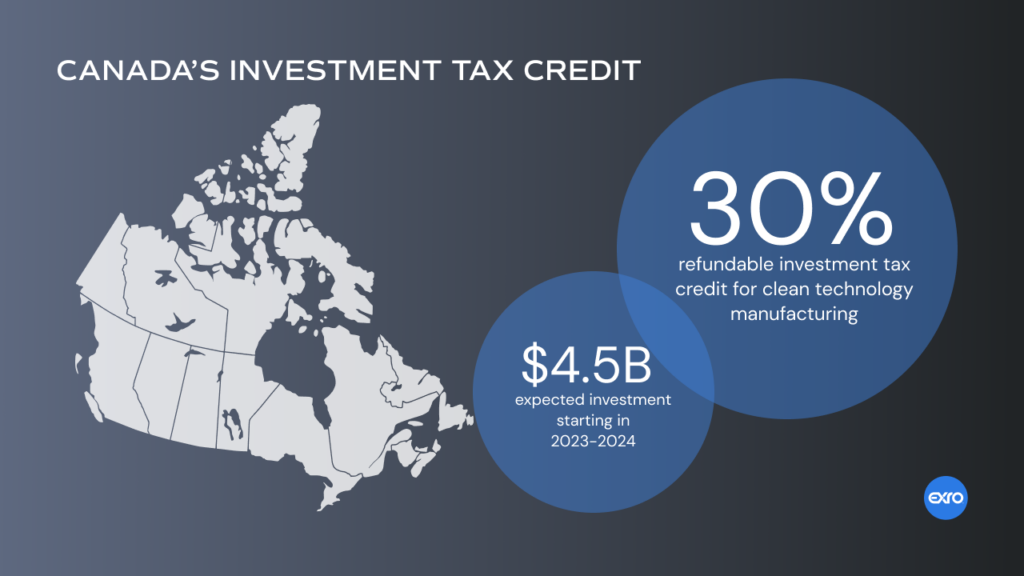

🍁Clean Technology Investment Tax Credit (CT ITC) — Quick Summary

The Clean Technology Investment Tax Credit (CT ITC) is a refundable federal tax credit that can reduce the net cost of eligible commercial solar and energy storage projects. The final credit depends on eligibility, timing (“available for use”), and labour requirements. For many businesses, CT ITC is one of the biggest levers in the commercial solar incentive stack—especially when combined with accelerated depreciation (CCA) and the right utility credit program.

Read the full CT ITC guide → https://magsolar.ca/clean-technology-investment-tax-credit-ct-itc/

Key Features of the CT ITC:

Refundable Nature: Unlike non-refundable credits that can only reduce tax liability to zero, the CT ITC ensures that if the credit amount exceeds the tax owed, the excess is refunded to the taxpayer.

Applicable Period: The credit applies to eligible property acquired and available for use between March 28, 2023, and December 31, 2034.

Variable Credit Rates: The credit rate is set at 30% for property available for use up to December 31, 2033, and decreases to 15% for property available in 2034.

Eligible Entities

Taxable Canadian Corporations: This encompasses most businesses operating in Canada, provided they are subject to Canadian corporate taxation.

Mutual Fund Trusts Classified as Real Estate Investment Trusts (REITs): These entities can also claim the credit, broadening the scope of eligible applicants.

Eligible Properties

The CT ITC is designed to support investments in specific types of clean technology properties. For businesses focusing on solar energy, the following are pertinent:

Solar Photovoltaic (PV) Systems: Equipment that harnesses sunlight to generate electricity.

Concentrated Solar Energy Equipment: Systems that use mirrors or lenses to concentrate a large area of sunlight onto a small receiver.

Stationary Electricity Storage Equipment: Such as batteries, provided they do not operate using fossil fuels.

Active Solar Heating Equipment: Systems designed to capture solar energy for heating purposes.

Requirements for Eligible Properties

Location: The equipment must be situated and used exclusively in Canada.

New Equipment: The property must be new and should not have been previously used or acquired for any purpose before its acquisition by the taxpayer.

Compliance with Standards: The equipment and its components must be certified by recognized certification organizations as mandated by relevant authorities.

Regulatory Adherence: All installations must comply with the Manitoba Electrical Code and any other applicable local laws and regulations.

💼 How Does This Incentive Compare to Other Commercial Solar Incentives in Canada?

The CT ITC is part of a broader suite of commercial solar incentives in Canada. When used in combination with other programs, the financial benefits become even more compelling.

Other Key Federal and Provincial Incentives:

Accelerated Capital Cost Allowance (ACCA) – Eligible systems under Class 43.1 or 43.2 allow businesses to write off their solar system faster (often 100% in the first year).

Clean Electricity ITC (upcoming) – Will provide up to 15% support for zero-emission electricity projects, separate from CT ITC.

Provincial Rebates – Some provinces like BC, Alberta, Manitoba, and Nova Scotia have rebate programs or grid credits via net metering.

By stacking the CT ITC with ACCA and local programs, you can reduce your total system cost by 50% or more.

🏙️ Use Case: How a BC Business Saved $76,500+

Let’s say a mid-sized commercial building in Vancouver, British Columbia wants to reduce long-term electricity overhead and stabilize energy costs and installs a 150 kW solar system at a cost of $250,000.

Here’s how the numbers might break down:

Clean Technology Investment Tax Credit (CT ITC): up to 30% refundable credit on eligible costs: Estimated CT ITC amount: $76,500

Accelerated Depreciation (ACCA Class 43.2): $205,000 write-off in Year 1

Estimated annual energy offset and savings: annual bill reduction range, $18,000–$28,000+

Payback Period: 5–10 years

IRR (Internal Rate of Return): 10%–14%

With these kinds of results, the Clean Technology Investment Tax Credit becomes a key reason why more companies are exploring commercial solar incentives in Canada.

🍃 Benefits Beyond the Tax Credit

Switching to solar isn’t just about reducing taxes—it’s about improving the long-term health of your business and the environment.

Strategic Advantages:

🌎 Meet ESG Goals: Align with global environmental standards

💡 Energy Independence: Hedge against rising utility rates

🏢 Boost Property Value: Solar increases real estate appeal

🛠️ Job Creation: Meeting labour requirements creates local skilled employment

💚 Brand Image: Customers increasingly choose eco-conscious companies

The CT ITC adds financial muscle to environmental leadership.

🧠 Final Thoughts: Why the CT ITC Matters

The Clean Technology ITC is a game-changing commercial solar incentive in Canada—not only because it saves you money, but because it accelerates your business’s path to sustainability and energy efficiency.

Whether you’re upgrading your current building or investing in new developments, this tax credit helps you:

Save on upfront capital costs

Reduce long-term operating expenses

Increase your environmental credibility

Strengthen your company’s bottom line

In short: you get rewarded for doing the right thing.

🏁 Summary

| Key Takeaway | Details |

|---|---|

| Focus Keyword | Commercial Solar Incentives in Canada |

| Primary Program | Clean Technology Investment Tax Credit (CT ITC) |

| Credit Amount | Up to 30% refundable |

| Eligibility | Canadian businesses & REITs |

| Bonus Incentives | ACCA (Class 43.1/43.2), Net Metering |

| Claim Deadline | Same as tax return (T2, T3, or T5013) |

| Labour Requirements | Prevailing wages + apprenticeships |

| Available Until | Dec 31, 2034 |

⚡Accelerated Investment Incentive (AII) for Commercial Solar (and why it matters)

In addition to the Clean Technology Investment Tax Credit (CT ITC), Canadian businesses investing in solar energy can take advantage of the Accelerated Investment Incentive (AII) — a powerful tool that allows you to depreciate solar equipment faster, increasing short-term tax savings and improving cash flow.

If you’re looking to stack your benefits from commercial solar incentives in Canada, this is a must-know.

📃 What “accelerated CCA” really means

Instead of deducting a small portion of the system each year, accelerated CCA rules can allow eligible businesses to deduct a much larger portion earlier — improving near-term cash flow and shortening the effective payback period.

🧾 What Is the Accelerated Investment Incentive (AII)?

The Accelerated Investment Incentive (AII) is a federal tax policy that gives businesses a bigger-than-usual tax deduction in the first year they purchase and use certain types of capital assets — including solar panels and related clean energy systems.

Under typical tax rules, you can only deduct a portion of the system’s cost each year through the Capital Cost Allowance (CCA). But with the AII, the first-year deduction is increased by up to 3 times the usual amount — putting more money back into your business sooner.

🛠️ How It Works

Here’s a simplified breakdown of how the AII boosts your CCA:

Normally, new assets are subject to the “half-year rule,” meaning you can only claim half of the first year’s depreciation.

With AII, that half-year rule is suspended, and instead:

You apply the full CCA rate to 1.5x the cost of the asset.

This means your first-year deduction can be 3x higher than under the regular rules.

For example:

If your solar equipment falls under a CCA class with a 20% rate, you’d normally deduct 10% in the first year due to the half-year rule.

With AII, you’d deduct 30% in the first year (20% × 1.5, with no half-year penalty).

This enhanced deduction only applies in the first year, but it frees up capital much earlier in the investment timeline.

💼 What Equipment Qualifies?

To use the AII for commercial solar installations, your system must meet these conditions:

✅ It’s considered eligible property (EP)

✅ It was acquired after November 20, 2018

✅ It became available for use before 2028

✅ It’s used exclusively in Canada and is new (not used or leased)

In many cases, solar PV systems, battery storage, and energy-efficiency upgrades installed by businesses fall under CCA Classes 43.1 and 43.2, which are actually fully expensed (more on that below). But the AII can still apply to related assets, including software, electrical upgrades, mounting structures, and other depreciable improvements.

🔁 How AII Works with Other Commercial Solar Incentives in Canada

Many businesses wonder: Can I use AII alongside the Clean Technology ITC? The answer is: yes — but not always in the same way.

Here’s how it works:

CT ITC gives you a refundable 30% tax credit on solar system costs.

CCA (including AII) allows you to deduct the remaining cost of the system from your taxable income.

However, any portion of your solar system cost covered by the CT ITC cannot also be deducted under CCA rules. So the general order of operations is:

Apply the 30% CT ITC

Reduce the cost of the system by the rebate amount

Apply AII or ACCA to the remaining balance

This creates a “stacking” effect where you:

Save 30% immediately (via CT ITC)

Deduct most of the remaining cost in Year 1 (via AII)

Reduce your tax bill even further over time

✅ This stacking structure makes the current era one of the most financially rewarding times to go solar in Canadian business history.

📉 How the AII Affects Future Depreciation

The AII front-loads your tax benefits, but it doesn’t increase the total deduction over time. That means:

You get more deductions early on, but fewer in later years.

The undepreciated capital cost (UCC) — the leftover balance for future deductions — will be smaller starting in Year 2.

For CCA classes that use straight-line depreciation (e.g., leasehold improvements), the percentages just shift around:

Year 1: 1.5× normal rate

Years 2–N: Lower deductions until cost is fully claimed

📌 Example: For a straight-line class with a 20% CCA rate and only one asset:

Year 1 deduction: 30%

Years 2–4: 20% per year

Year 5: 10% (final balance)

📉 Phase-Out of the AII After 2023

The AII is not permanent. It’s gradually phasing out starting in 2024.

| Year Property Becomes Available | First-Year Deduction Multiplier |

|---|---|

| 2018–2023 | 3x (full AII) |

| 2024–2027 | 2x (reduced AII) |

| 2028+ | AII no longer available |

If you’re planning a commercial solar project, there’s a limited window to access the full benefits of the AII. Starting your project soon helps you maximize tax savings.

✅ Key Takeaways on the Accelerated Investment Incentive

| Benefit | Summary |

|---|---|

| 📅 Available Until | End of 2027 (full benefit until 2023) |

| 💸 First-Year Deduction | Up to 3x normal CCA amount |

| ⚙️ Applies To | Eligible new property (hardware, improvements, etc.) |

| 📉 Impact on Future Years | Lower UCC = lower future deductions |

| 🧾 Compatible With | CT ITC, Class 43.1/43.2, ACCA |

| 🧠 Strategy | Stack with CT ITC for maximum solar ROI |

📉 In practical terms: AII can meaningfully improve the “year-one” depreciation profile for eligible commercial solar assets, but the exact effect depends on:

when the system becomes available for use,

which CCA class your equipment qualifies under,

- and whether any other tax rules apply to your specific entity structure.

Why CFOs care (even if they don’t love solar)

CCA isn’t a “rebate” — it’s a tax deduction mechanism. But it can change the internal financial picture because it improves:

near-term cash flow,

after-tax returns,

- and the project’s IRR/NPV (depending on your assumptions).

Important: Your accountant should confirm eligibility, classing, and claim strategy based on your business structure and the final scope of equipment installed.

🌞 Provincial & Utility Programs

(How Your Savings Show Up on the Bill)

Federal incentives can reduce project cost and improve after-tax returns — but your utility program determines how solar savings actually appear month to month. This is why commercial system design should match local rules around exporting energy, crediting, rate structures, and annual true-ups.

Alberta (Micro-generation / crediting mechanics)

In Alberta, many commercial solar projects in Calgary and Edmonton areas are fit under the micro-generation framework, where your system offsets on-site electricity first, and any surplus exported to the grid becomes bill credits through your retailer. The way those credits appear (and when/if unused credits are settled) can depend on your retailer and account structure, which is why it’s important to confirm the “real” bill mechanics before final sizing.

Practical design note: Alberta projects are often optimized around annual consumption, export behavior, and rate structure so you don’t oversize a system that creates “paper savings” instead of real financial value.

British Columbia (BC Hydro self-generation + larger-project considerations

In BC, many commercial systems fall under BC Hydro’s self-generation pathways, designed for customers generating renewable electricity primarily for their own use. The value of solar depends heavily on your building’s load profile (daytime usage is ideal), and on how surplus exports are treated under program rules and capacity thresholds. For larger projects, interconnection and program requirements can become more specific, and project economics may shift depending on export limits and how the utility credits energy over time.

Practical design note: the best ROI usually comes from sizing to your building’s usage pattern and confirming how surplus energy is credited—especially if your site has seasonal loads or plans to expand.

Manitoba (Net Billing — monetary credits, not 1:1 kWh banking)

Manitoba Hydro uses net billing (not traditional 1:1 net metering). That means your solar offsets your building’s usage first, and surplus electricity exported to the grid is credited as a monetary credit on your account rather than “banked” as kWh at the retail rate. This difference matters a lot for commercial payback, because the export value may not match what you pay for electricity.

Practical design note: Manitoba projects are usually designed to maximize on-site self-consumption and avoid oversizing—because the financial return is typically strongest when your solar production lines up with your facility’s demand.

Nova Scotia (Commercial Net Metering)

Nova Scotia Power offers Commercial Net Metering, which allows eligible customers to generate renewable electricity to offset a portion (or all) of their consumption, with surplus energy credited for future bills under the program structure. In practice, program details like credit banking rules, annual reconciliation/true-ups, and system sizing limits can affect the business case—especially for facilities with seasonal operations or variable loads.

Practical design note: net metering policy details matter for payback, so the safest approach is sizing the system to match your annual usage and confirming the program rules that apply to your specific meter and rate class.

MAG Solar can quickly confirm which pathway fits your building and size the system around the rules that actually control the financial outcome.

🧑💼 How CFOs Model Commercial Solar ROI

(What Decision-Makers Actually Look At)

If you’re pitching commercial solar internally, it helps to understand how CFOs and finance teams typically think. They’re not just asking “Will it save money?” They’re asking whether solar is a good capital allocation decision compared to other uses of cash, and whether the assumptions are reliable.

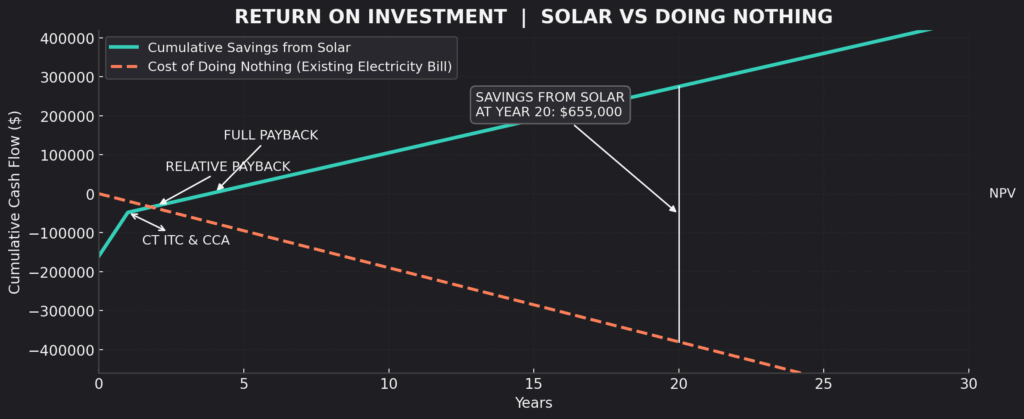

Start with the baseline: “What happens if we do nothing?”

The cleanest way to model ROI is to compare two paths:

Do nothing: keep paying the utility bill for the next 20–30 years

Go solar: pay for an asset up front (or finance it) and reduce the utility bill over time

This “solar vs doing nothing” comparison frames solar as a hedge against long-term energy cost risk — not just a feel-good sustainability project.

This “solar vs doing nothing” comparison frames solar as a hedge against long-term energy cost risk — not just a feel-good sustainability project. We cover more in our full guide here.

📊 Use multiple metrics (not just payback)

Payback is easy to understand, but CFOs usually want a few perspectives:

📈 Simple Payback

The year your cumulative savings equal your net installed cost. It’s intuitive, but it ignores the time value of money.

⏳ Internal Rate of Return (IRR)

IRR estimates the annualized return of the project. It helps CFOs compare solar to other investments or capital projects.

💰 Net Present Value (NPV)

NPV discounts future savings back to today’s dollars. CFOs like NPV because it answers a direct question: “Is this investment worth more than it costs, in today’s terms?”

⚡ Levelized Cost of Energy (LCOE)

LCOE estimates the all-in cost to generate a kWh with solar over the system’s life. It’s useful for comparing solar electricity to grid electricity over the long run. You don’t need all of these for every project, but the more sophisticated the buyer, the more likely you’ll want to include at least NPV + IRR in your model.

🧠 The assumptions that matter most

Most commercial solar models are won or lost on a few key assumptions. The best practice is to keep these transparent and conservative:

💸 Electricity rate assumptions

Many models include an annual escalation rate for electricity costs. Even small differences here can change long-term results, so CFOs will want to see a conservative scenario and a higher-cost scenario.

🌞 Production assumptions (annual kWh)

Annual kWh depends on roof layout, shading, tilt, azimuth, and real-world losses. Good models include realistic performance assumptions rather than “perfect lab” outputs.

🔁 Export credit value (this can make or break ROI)

This is huge. Your utility program determines how exported energy is credited, how credits carry forward, and whether there are annual true-ups. A system can look amazing on paper but disappoint if exports are valued differently than expected. This is why sizing to the load profile matters.

🧱 Solar changes the risk profile (and CFOs like that)

A lot of finance teams view solar as “boring in a good way.” It can reduce exposure to unpredictable utility costs by converting part of your energy spending into a predictable asset return. That risk reduction is hard to capture in a simple payback number — but it’s often the reason the project gets approved.

A simple internal model structure that works

If you’re building a basic CFO-ready business case, a simple structure looks like this:

Total installed cost (and what’s included)

Estimated incentive impact (credits/rebates where applicable)

Net project cost after incentives

Year 1 production estimate (kWh) and bill offset estimate

Export credit assumptions (based on your province/program)

O&M allowance and performance decline

Outputs: payback + NPV + IRR under conservative and base scenarios

If you want the fastest path to an accurate business case, MAG Solar can produce a preliminary model based on your site, your load profile, and the utility rules that control how savings show up on the bill.

👷 MAG Solar’s process for commercial projects

Because commercial solar touches engineering, finance, incentives, and operations, our process at MAG Solar is intentionally structured and transparent.

Step 1 – Discovery and data collection

We start with:

- 12–36 months of interval or billing data (where available)

- Recent utility bills and tariff details

- Roof drawings or satellite imagery

- Basic information about your business, operating hours, and goals

From here, we develop a high-level feasibility scan, so you’re not guessing whether the project is even worth deeper analysis.

Step 2 – Preliminary design and capacity study

Our design team builds an initial layout:

- Array size and orientation based on roof or land constraints

- Preliminary production estimates using bankable solar modelling tools

- Early thoughts on structural and electrical considerations

This gives you a first look at what’s physically possible.

Step 3 – Incentive and financial modelling

We then layer in:

- CT ITC eligibility for your corporate structure and project timing

- Accelerated CCA treatment and the accelerated investment incentive

- Provincial programs such as Solar Club, BC Hydro Self-Generation, BC Hydro Load Displacement, and CEIP where applicable

We model multiple scenarios (e.g. different system sizes, cash vs financing options) so your finance team can compare payback, IRR, NPV, and cash-flow profiles side by side.

Step 4 – Detailed engineering and interconnection

Once you approve a direction, MAG Solar proceeds with:

- Third Party structural engineering sign-off and any required upgrades

- Detailed electrical design and protective device coordination

- Utility interconnection applications and any required studies

- Final equipment selection (modules, inverters, racking, monitoring)

Independent and licensed, electrical and structural engineers work together so that the design is not only efficient, but fully compliant with code and utility requirements.

Step 5 – Construction, commissioning, and training

During construction, our project managers coordinate:

- Site access, cranes, and safety equipment

- Roof protection and sequencing to minimize disruption to operations

- Installation of racking, modules, wiring, and switchgear

- Testing, commissioning, and utility witness (where required)

We then walk your team through:

- System operation basics

- Monitoring portals and reporting

- What to expect on your first few utility bills

Step 6 – Ongoing performance and support

Commercial solar is a 25+ year asset. MAG Solar provides:

- Performance monitoring and alerting

- Support in interpreting production data vs. expectations

- Guidance when tariff structures, incentives, or operational needs change

Our goal is not just to install a plant, but to ensure that it continues producing the financial and sustainability outcomes you modelled at the start.

🚀 Why AII Matters for Commercial Solar Incentives in Canada

In the current landscape of commercial solar incentives in Canada, the AII serves as a strategic tool that complements the CT ITC. By accelerating your depreciation and combining it with tax credits and potential provincial rebates, the total effective cost of going solar could be reduced by over 50%.

For CFOs, sustainability officers, and property developers, this creates a rare opportunity to future-proof operations, reduce emissions, and improve financial performance — all while accessing one of the most favorable incentive environments Canada has ever offered.

- Let's Connect

Get a Free Commercial Solar Assessment

See How Much you Can Save with Commercial Solar. Get your Free Design & Consultation

📞 Ready to Take Advantage of Commercial Solar Incentives in Canada?

See if your Qualify

With generous programs like the Clean Technology Investment Tax Credit (CT ITC) and the Accelerated Investment Incentive (AII), there has never been a better time to invest in solar. These commercial solar incentives in Canada can help your business lower operating costs, reduce emissions, and boost long-term ROI.

At Mag Solar, we specialize in helping Canadian businesses navigate and maximize these incentives—from consultation to installation and everything in between. Fill out the form below to see if you qualify! 👇

Commercial solar incentives in Canada typically include federal incentives (like the Clean Technology Investment Tax Credit and accelerated depreciation through clean energy CCA classes), plus provincial and utility programs that determine how your savings show up on your bill (net metering, net billing, self-generation rules, export credits, and true-ups). The “best” incentive mix depends on your province, utility, and building load profile.

Commercial solar incentives in Canada can reduce the total cost of a solar project by 30% or more through refundable tax credits, capital cost deductions, and sometimes even provincial rebates. These savings improve your return on investment and shorten the payback period of commercial solar installations.

Eligible businesses include:

-

Taxable Canadian corporations

-

Commercial landlords and developers

-

Real Estate Investment Trusts (REITs)

-

Partnerships where all members are eligible corporations

As long as your project is in Canada and involves new, qualifying clean energy equipment, you may be able to access commercial solar incentives in Canada.

Yes — solar panels are one of the main technologies supported under commercial solar incentives in Canada. Both grid-tied and off-grid solar PV systems, solar heating, and concentrated solar equipment can qualify for the CT ITC and accelerated capital cost deductions.

Absolutely. You can combine:

-

The CT ITC (30% refundable tax credit)

-

The Accelerated Investment Incentive (AII)

-

The Accelerated Capital Cost Allowance under Class 43.1 or 43.2

-

Provincial solar rebates (where available) Stacking these commercial solar incentives in Canada can reduce your net project cost by 50% or more.

he CT ITC is a federal refundable tax credit that can materially reduce the net cost of eligible commercial solar and energy storage projects. Because it’s refundable, it can be one of the most impactful incentives for businesses — but the final outcome depends on eligibility, timing, and compliance requirements. Many strong commercial ROI models treat CT ITC as a core pillar of the incentive stack.

The Accelerated Investment Incentive is another powerful tool within the suite of commercial solar incentives in Canada. It lets businesses deduct up to 3 times the normal depreciation in the first year for eligible solar equipment. This improves short-term cash flow and makes commercial solar more affordable.

Yes. Businesses can stack the CT ITC with:

-

Accelerated Capital Cost Allowance (ACCA) under Classes 43.1 and 43.2

-

The Accelerated Investment Incentive (AII)

-

Provincial rebates or net metering programs

Stacking incentives can dramatically reduce your net project costs and improve ROI.

These terms often get mixed together. In simple terms, accelerated depreciation strategies can let businesses deduct eligible clean energy equipment faster, which improves after-tax cash flow. The exact mechanics depend on the class the equipment falls under and the current tax rules that apply to your entity and timing. Your accountant should confirm the best approach for your situation.

Yes — this is called a recapture. If you:

-

Sell the solar equipment

-

Export it outside Canada

-

Convert it for non-clean tech use

…within 10 years of claiming the credit, you may need to repay all or part of the CT ITC.

Eligible projects include:

-

Solar rooftops for commercial buildings

-

Ground-mounted solar farms for businesses

-

Solar parking canopies

-

Off-grid commercial solar with battery backup

-

Solar for industrial warehouses, retail plazas, or agricultural operations

The system must be new, certified, and installed in Canada by licensed professionals.

Battery storage can qualify under some incentive frameworks and can improve project value when it supports resilience, export control, or demand management. However, batteries don’t always maximize ROI in the same way solar does on its own, so the best approach is to model storage based on your actual objective (backup power, peak shaving, operational continuity, etc.).